Theoretical value of a call

Theoretical value of a callThis model, developed to evaluate currency options, considers foreign currencies analogous to a stock providing a known dividend yield. The owner of foreign currency receives a “dividend yield” equal to the risk-free interest rate available in that foreign currency. The model assumes price follows the same stochastic process presumed in the Black-Scholes model.

This model is used to evaluate options written on currencies. The interest rate of the native currency is used as the default, but you can set the foreign interest rate in Model preferences.

This model corrects the difference between native and foreign interest rates. However, as a modification of Black-Scholes model, it possesses all its limitations.

Notation

Theoretical value of a call

Theoretical value of a put

Theoretical value of a put

Underlying price

Underlying price

Strike price

Strike price

Interest rate

Interest rate

Interest rate in the foreign country

Interest rate in the foreign country

Time to expiration in years

Time to expiration in years

Volatility

Volatility

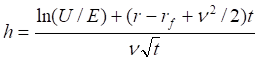

The European call price is given by:

Where:

The European put price is given by: