The Ho-Lee model (1986), an interest rate model is the no-arbitrage model. The model allows closed-form solutions for European options on zero-coupon bonds.

TheoV

Call

Put

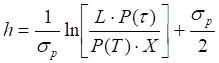

Where

L – bond principal (i.e. face value),

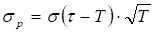

τ – bond time maturity,

,

,

,

,

P(T) - the price at time zero of a zero-coupon bond that pays $1 at time T,

The distinctions from Vasicek model are

- PT and Pτ are input parameters,

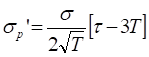

- σp expression is different.

Delta

Call

Put

Gamma

Gamma is identical for put and call options.

Vega

Because

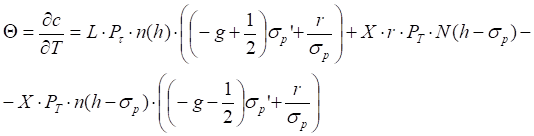

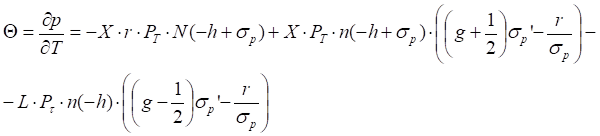

Theta

Call

Put

where

,

,

Rho

Since the price at time zero of a zero-coupon bond that pays $1 at time t is

then

then

Call

Put

Implied volatility

The system finds implied volatility numerically.